Requiem for Alan Greenspan the Bubble Master

Greenspan enthusiastically promoted the deregulation that characterized the era of high neoliberalism.

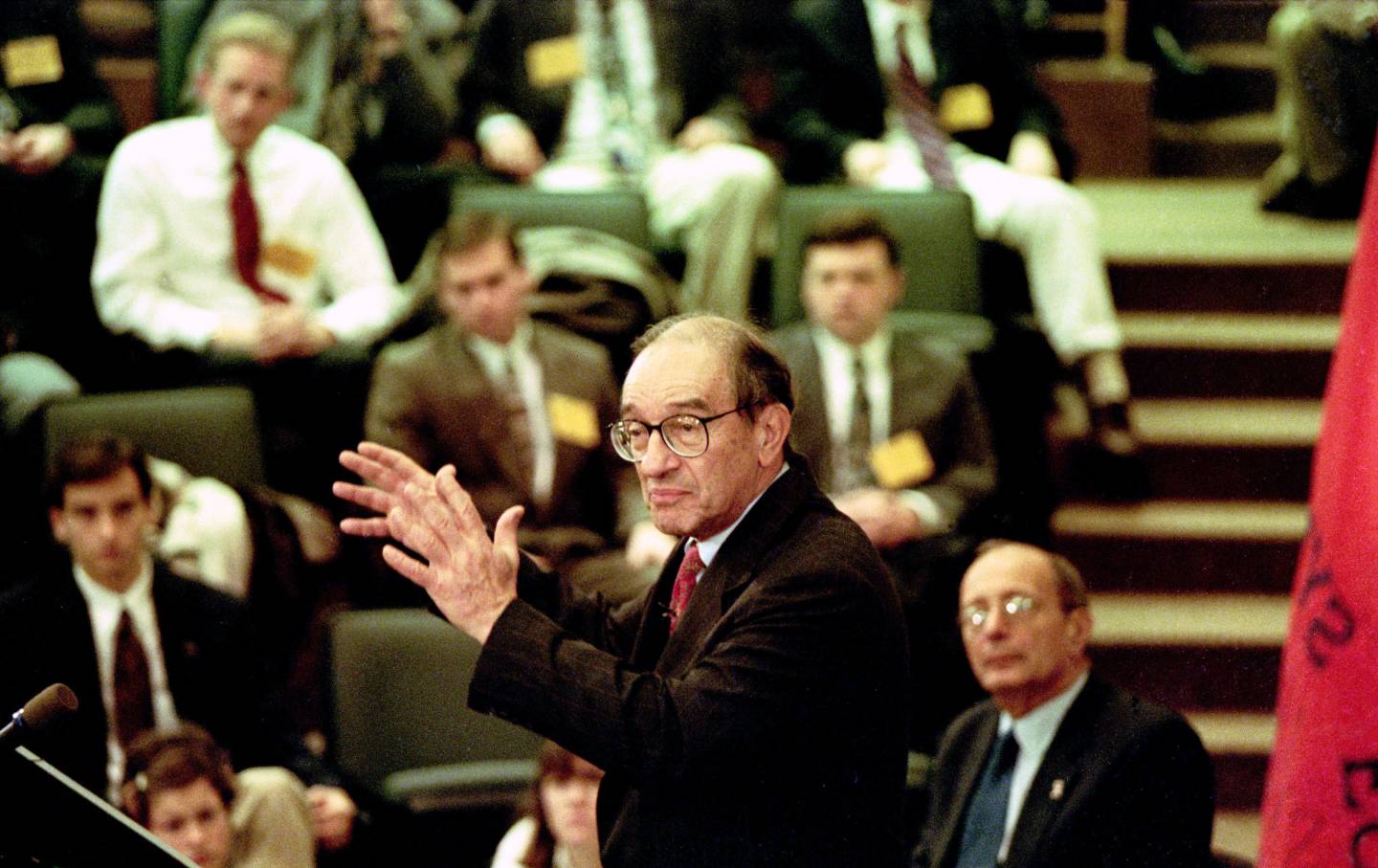

Alan Greenspan, an early follower of Ayn Rand who rose through Republican political circles to become chair of the Federal Reserve from 1987 to 2006, has died at the age of 100. In this, he matched fellow ruling-class ghoul Henry Kissinger, though it must be conceded that Kissinger had more blood on his hands than Greenspan, whose major crimes were in economic management, not mass murder. But both were treated with undeserved admiration in life and death. Let’s see what we can do about correcting Greenspan’s record.

As a young economic consultant in New York in the late 1950s, Greenspan fell into wacko libertarian Rand’s circle and began to preach her gospel: Markets are great; government stinks; winners should be rewarded generously, and losers punished with no pity. When her massive novel Atlas Shrugged was published to mostly bad reviews in 1957, Greenspan defended it in a letter to The New York Times as “a celebration of life and happiness.” But while her worldview might seem harsh to the uninitiated, “justice is unrelenting,” and those who won’t get with the free-market program have only themselves to blame if they fail to prosper. As Greenspan put it, “Parasites who persistently avoid either purpose or reason perish as they should.”

In his days with the cult, he denounced the creation of the Fed, an institution he would later head for longer than anyone else, as a “historic disaster,” because it removed the discipline of the gold standard. The beauty of gold is that it puts severe limits on the growth of money and credit, thereby putting a limit on speculative bubbles of the sort he would later preside over.

Greenspan soon found his way into Republican politics, trying to push Richard Nixon in a libertarian direction that Nixon wasn’t too keen on because it would have been politically suicidal. It wasn’t an ideal role for the Randian in him, but the Rand circle itself was falling apart, and he’d discovered that counseling a president “could be an addictive habit,” as his biographer Sebastian Mallaby put it.

Nixon nominated him to be his chief economic adviser in 1974, just before his resignation. Greenspan’s confirmation hearings were stormy, given his history of libertarian provocations, but he won over skeptical senators, including Joe Biden, who found him sharp and honest despite his politics. By the time Greenspan was confirmed and sworn in, Nixon had resigned and Gerald Ford was president. One of the few guests at the swearing-in was Ayn Rand.

Enjoying his taste of power, Greenspan accommodated himself to the inevitable compromises of political life. Although he would later view his Randian period as a youthful phase, he never dropped his faith in what Ronald Reagan liked to call “the magic of the marketplace.”

After Ford left office, Greenspan went back to the economic consulting firm he’d headed since 1955; he’d stay there until Reagan appointed him chair of the Fed in 1987. Two months after he took charge at the Fed, the stock market staged one of the greatest crashes in history. Greenspan ignored the Randian scripture and instead issued a statement that would become the canonical response to a financial crisis in the ensuing decades: “The Federal Reserve, consistent with its responsibilities as the nation’s central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.” In other words, we’ll pump money into the system to keep things from imploding. This is the very opposite of the gold standard Greenspan once touted, but he had a real economy to run. Markets stabilized, and after a few months it seemed as if almost nothing had happened. The reaction gave rise to a new Wall Street aphorism: “bailouts are bullish,” an aphorism whose truth would be proved many times over the next four decades.

Unlike under his predecessor, Paul Volcker, Greenspan’s Fed was not a regime of austerity, characterized by tight money and high unemployment. The average unemployment rate during Greenspan’s tenure was more than two percentage points lower than it was under Volcker; the maximum was three points lower. Contradicting orthodoxy, Greenspan didn’t raise interest rates to fight inflationary pressures as the unemployment rate fell below 5 percent in the late 1990s; he believed that the technological revolution had kicked up productivity growth to the point where inflation was no longer a danger. Also, in his view, high unemployment wasn’t necessary to scare the working class into submission; years of downsizings had produced a fear of job loss that left workers feeling deeply insecure “despite the tightest labor markets in decades,” as he put it in a July 2000 speech. Workers felt like the unemployment rate was a couple of points higher than the actual rate of 4 percent, and that was fine with him since it kept wages down.

But that easy-money policy had encouraged inflation of another kind, in stock prices. The market reached heights not seen since the 1920s and then some. (We’ve since left those records way behind.) From the low after the 1987 crash to the eventual high in March 2000, the market rose almost 450 percent, a run with few historical precedents. Along the way, Greenspan did worry that maybe things were getting out of hand. In a 1996 speech, he famously wondered if an “irrational exuberance” had taken things over, but Wall Street—which had fallen in love with the exuberance, irrational or not—did not receive his remarks well and he didn’t bring up the subject again for years. The market would double from the day of that speech until its 2000 peak.

Greenspan and his irrationally exuberant stock market were central to the giddy triumphalism of the Clinton era. For a few magical years, it seemed like recessions and even class conflict were things of the past. But they weren’t. The bubble burst, as bubbles always do, and while a classic depression didn’t take hold thanks to Greenspan’s policy of extended low interest rates, neither did prosperity. Following the brief recession in 2001, there was a “jobless recovery” that still felt like a recession to most people.

Low interest rates did, however, encourage a new bubble, this time in housing. House prices, which had been rising gently in the late 1990s, showed no ill effects from the stock market’s troubles—in fact, their rise would soon accelerate to a highly exuberant pace. Throughout, Greenspan showed little concern. As he said in a 2004 speech, while a number of analysts have worried that “the extended period of low interest rates is spawning a bubble in housing prices in the United States that will, at some point, implode,” this did “not seem the most probable outcome,” because “nominal house prices in the aggregate have rarely fallen and certainly not by very much.” He revised his thinking somewhat in June 2005, conceding that while there was no “bubble” proper, there were “signs of froth in some local markets where home prices seem to have risen to unsustainable levels.” Froth, as every beer drinker knows, is a collection of small bubbles, so this may have been a distinction without a difference.

The subsequent crash in house prices and the mortgage bonds that made the boom possible gave rise to the financial crisis of 2008 and the worst recession since the 1930s. It also threw Greenspan into an intellectual crisis. He simply could not believe markets could have been so wrong, that bankers would have made so many bad loans and investors made so many bad investments. Of course, those things happen, which is why the financial sector had historically been highly supervised and regulated, but Greenspan enthusiastically promoted the deregulation that characterized the era of high neoliberalism. When confronted by Representative Henry Waxman at a hearing on the financial crisis, Greenspan waffled some about whether he’d been wrong about deregulation but conceded that he’d been very “distressed” by discovering “a flaw in the model that I perceived is the critical functioning structure that defines how the world works, so to speak…. I was shocked, because I had been going for 40 years or more with very considerable evidence that it was working exceptionally well.” Until it didn’t.

Popular

“swipe left below to view more authors”Swipe →Greenspan wasn’t alone in this “shocking” discovery. But the insight didn’t last and it was back to super-low interest rates and fresh bubbles. House prices went on a tear in the years after the pandemic and the stock market has been a hotbed of exuberance for most of the last 15 years. Meanwhile, real economic problems, like insecurity and pinched living standards, were ignored. No one in public life thinks about how to keep unemployment low and workers secure without encouraging the growth of bubbles, which contribute greatly to increased wealth inequality and then produce widespread damage when they inevitably burst.

Greenspan’s model lives on.

More from The Nation

The War on the UAW The War on the UAW

The United Auto Workers called for a ceasefire in Gaza. The union’s federal monitor didn’t like it—and now he’s investigating Shawn Fain, just weeks before union elections.

How Public Equity Can Promote a Revived American Democracy How Public Equity Can Promote a Revived American Democracy

Critics are assailing deals to give the government stakes in major companies—but they’re overlooking their civic dividends.

The Trump Administration Is Making It Nearly Impossible to Get Food Stamps The Trump Administration Is Making It Nearly Impossible to Get Food Stamps

New work requirements and restrictions on SNAP have kicked millions off the benefit rolls, with more reductions to come.

What Is the American Economy? What Is the American Economy?

The gap between what the numbers say and how people are feeling has only grown wider.

Why Amazon Ditched Its Prestige Sam Altman Biopic Why Amazon Ditched Its Prestige Sam Altman Biopic

Artificial had a roster of premier talent and a topical subject—but it no longer fit in with Jeff Bezos’s financial ambitions.

What Should Be Done With America’s Slave Mansions? What Should Be Done With America’s Slave Mansions?

A case for reimagining plantations—the engines of centuries of oppression—as laboratories for economic justice.