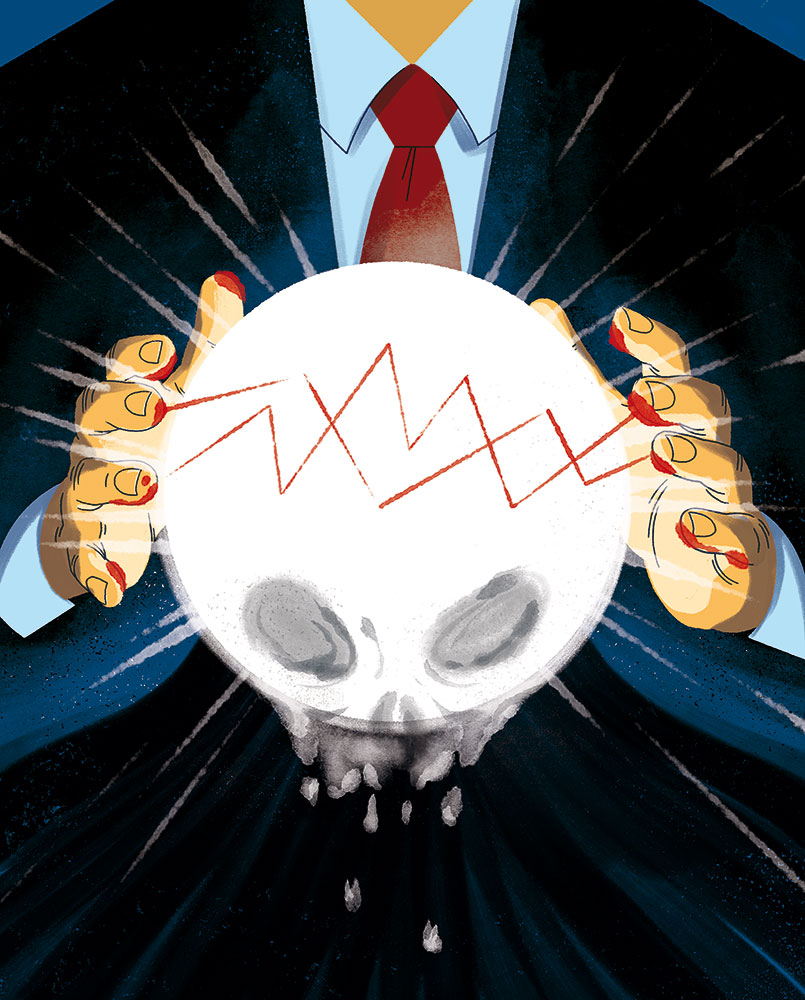

How Prediction Markets Are Taking Control of Everything

We have seen the future, and it is Polymarket and Kalshi processing insider bets on mayhem, chaos—and celebrity-wedding guest lists.

Prediction markets—online casinos disguised as investment vehicles, where you can bet on propositions ranging from who will win a particular sports contest to who will be a bridesmaid at Taylor Swift’s wedding—have exploded in the past two years. The monthly trading volume among prediction wagerers has skyrocketed, from $1.2 billion in early 2025 to more than $20 billion in January 2026, according to the blockchain-research firm TRM Labs. The two largest prediction markets, Polymarket and Kalshi, have a combined valuation north of $30 billion, making their founders some of the world’s most improbably young billionaires.

Most Americans who know of these strange hybrid beasts—half futures markets, half slot machines—likely encountered them in one of two ways: in news reports on their use as a tool for political insiders to make easy money wagering on war and death, or by discovering their capacity as a backdoor way to bet on sports in states like California and Texas that haven’t legalized sports gambling.

The war-and-death contracts landed with particular force in early January, when a Polymarket account likely created a week before US forces seized Venezuelan President Nicolás Maduro turned a $33,000 bet on his removal from office into $400,000 in profit, with two other accounts of apparent insiders collectively clearing another $230,000. The timing was difficult to explain without invoking advance knowledge of a military operation so secret that top members of Congress hadn’t been briefed on it.

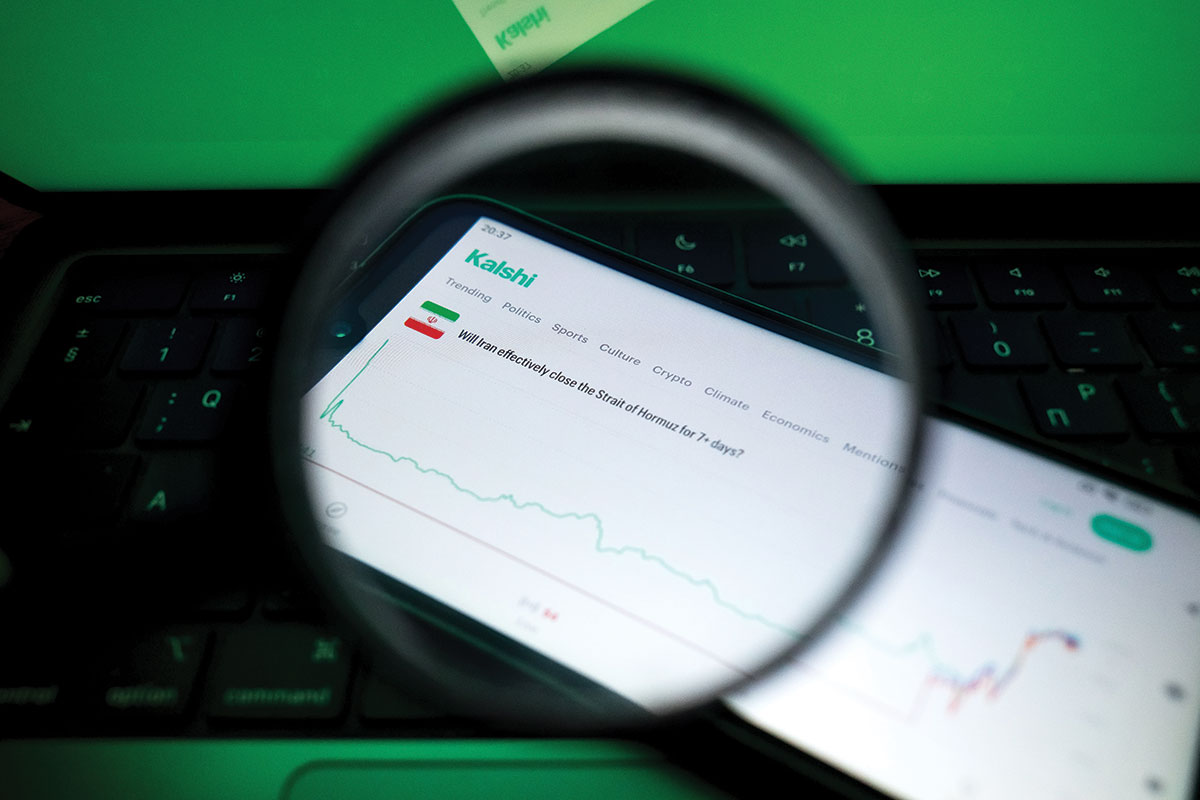

And then there was Iran. Starting in December, Polymarket booked more than $529 million in bets on whether or when the United States would strike Iran; Kalshi allowed $54 million in bets on when Ayatollah Ali Khamenei would be removed from power, which turned out to mean killed in the joint US-Israeli air strikes on February 28. The New York Times found that in the 24 hours before the strikes, over 300 bets of at least $1,000 flooded in, with at least 16 accounts clearing more than $100,000 each; one account turned $60,000 into nearly half a million. A trader going by the name “Magamyman” made more than $553,000; another suspiciously lucky Polymarket patron had taken in nearly $1 million on a series of stunningly accurate bets on US and Israeli attacks on Iran over several years, according to CNN. (Kalshi, awkwardly claiming that it didn’t allow betting on death, canceled all of the wagers and issued refunds, infuriating the traders who had predicted correctly.) Connecticut Democratic Senator Chris Murphy was blunt: “I think it’s likely there were people making the decision on war with Iran that had a financial interest in doing so because they had placed a bet on one of these markets. It’s worse than insider trading.”

The early days of the Iran war also saw a distressing example of how the prediction markets’ penchant for death-betting could take a dangerous, wag-the-dog turn. Emanuel Fabian, a reporter for The Times of Israel, fielded a stream of ever more urgent messages from online accounts demanding that he alter a report he’d filed on a March 10 Iranian missile attack on Israel; they wanted him to say that the fallen ordnance in question were fragments brought down when Israel intercepted the Iranian missile in the air. It turned out that many Polymarket bettors had bet “no” on March 10 as the date for Iran’s first successful missile attack on Israel, and an intercepted missile meant the strike didn’t count. Angry Polymarket users passed around a doctored screenshot that supposedly showed Fabian walking back his story; one distressed bettor who had staked $900,000 on his “no” bet threatened Fabian’s life and claimed to know the whereabouts of his family.

Polymarket, for its part, has defended its war markets as an “invaluable” source of information and insight, issuing a surreal statement celebrating “the wisdom of the crowd” and claiming that “after discussing with those directly affected by the attacks, who had dozens of questions, we realized that prediction markets could give them the answers they needed in ways TV news and X could not.” Sure, Jan. But as unbelievable as such a claim may sound, it signals something important: The prediction-market project is not only about business. It’s also ideological. “Kalshi is replacing debate, subjectivity, and talk with markets, accuracy, and truth,” the company’s cofounder and CEO, Tarek Mansour, declared in a press release with typical tech bravado, as if the fervid speculations of a legion of hyped-up crypto-bro gamblers are anything other than subjective. “We have created a new way of consuming and engaging with information. It’s hard to have an opinion about the future today without thinking about Kalshi.” And that’s the problem in a nutshell: Mansour and the other leading apostles of the prediction market have ambitions that go far beyond war and Taylor Swift. Mansour says that his aim is “to financialize everything and create a tradable asset out of any difference of opinion.” The intellectual godfather of prediction markets, George Mason University economist Robin Hanson, wants to push things even further, touting them as a kind of replacement for democracy, one capable of taking over much of the machinery of government.

To understand what this brave new world will actually look like, you first have to understand what online sports betting has already done to us.

In 2018, the Supreme Court struck down a federal law banning sports gambling in all states but Nevada. What followed was a digital gold rush. State legislatures, facing perennial budget shortfalls, fell over themselves in the effort to legalize and regulate—and tax. Harry Levant, a former Philadelphia attorney and recovering gambling addict who has become a leading advocate for federal gambling reform, puts it bluntly: “They were becoming addicted—and I use the word intentionally—to the idea of finding a new source of revenue. If my neighboring state has it, we have to have it too.” Within a few years, 39 states had legalized some form of sports gambling, and millions of Americans proceeded to collectively lose somewhere in the vicinity of $50 billion chiefly just by staring at their phones.

The product that those (mostly) men were staring at was not quite what state legislators had voted for. Beginning in 2021, the major sports leagues started selling granular real-time data to the betting industry to enable “prop” (or proposition) bets on every micro-event in a game, no matter how seemingly trivial. As Levant puts it: “These elected officials had no idea we were going to be allowing betting on the speed of every tennis serve.”

If you’re a sports fan, you may have some idea of what happened next, but you may still be a little taken aback by the full extent of the transformation. In 2017, before the Supreme Court’s decision, wagerers staked $4.8 billion in legal bets on sports. Last year, that figure reached $167 billion.

Nearly half of American men between 18 and 49 have an online sports-betting account, according to a 2025 poll by the Siena College Research Institute. Sports media has been thoroughly colonized: Gambling commentary is woven into broadcasts, ad breaks are dominated by FanDuel and DraftKings, and much of sports radio has become an extended advisory service for would-be bettors.

It’s not exactly rare for sports fans to consider themselves experts on the subject. And so it’s hardly surprising that the average sports bettor, confident in their knowledge, expects to come out modestly ahead over time. A Stanford University study found that this belief is nearly universal—and nearly universally wrong, with nine in 10 bettors overestimating their chances of winning. The cold reality is that 96 percent will lose money in the long term.

But it’s not just about overconfidence. Sports-betting apps, living on the phones we always have with us, are “addictive by design,” to paraphrase the title of New York University anthropologist Natasha Dow Schüll’s influential book on gambling technology. Jonathan D. Cohen, the author of Losing Big: America’s Reckless Bet on Sports Gambling, describes them as potent dopamine-delivery systems—like social-media apps, only more so—“where there’s an endless array of things to bet on, and the lines on a game update constantly so that you can just endlessly scroll.”

Schüll, who cut her teeth studying slot machines in Vegas, takes me through the similar mechanics of sports-gambling apps in a phone interview: variable rewards, continuous action, fast feedback, and, crucially, no resolution—because when one game ends, you can simply move on to another. After the last buzzer in a US sports competition has sounded for the night, eternally hopeful bettors hunker down in their rooms, bathed in the glow of their phones, chasing opportunities across time zone after time zone and sport after sport, wagering on everything from Ugandan basketball to Belarusian soccer. They don’t even have to take breaks to eat or go to the bathroom. Levant, who now counsels gambling addicts, tells me, “I have patients who take their phones into the shower with them.” At least they’re still showering.

The cheerful sportsbooks ads belie a considerably darker reality. A UCLA study found that states that legalized online sports betting saw bankruptcy filings rise by 27 percent, debt sent to collections increase by 8 percent, and credit scores fall three times faster than in states with only in-person betting, with these effects concentrated most heavily among lower-income households. Fifteen percent of Maryland adults who have gambled on sports in the past year suffer from disordered gambling, a condition that heightens reckless betting behavior while foreshortening the awareness of its consequences, according to a 2025 University of Maryland School of Medicine survey. And the damage isn’t just financial: A University of Oregon study found that legalized sports betting amplifies the already documented spike in intimate-partner violence that follows an unexpected sports loss.

The industry’s acknowledgment of all the baleful side effects of its addiction-based business model is laughably perfunctory. DraftKings launched a “responsible gambling” campaign last year set to Kenny Rogers’s “The Gambler.” The tagline? “It’s more fun when it’s for fun.”

The intellectual origins of prediction markets go back, improbably, to a county fair in Plymouth, England, in 1906. Francis Galton, the Victorian polymath and OG eugenicist, wanted to prove that ordinary people were bad at reasoning. So he collected 800 entries from a competition to guess the weight of a slaughtered ox and calculated the median estimate: 1,207 pounds, a mere nine pounds over the actual weight. The crowd was clearly on to something. Galton published the humbling result in Nature. The idea that the “wisdom of crowds” can be more accurate than expert opinion can be traced back directly to that dead ox.

Fast-forward to 1988, when Robin Hanson, then a researcher working at Lockheed, had an idea: What if you could design markets that harvested that collective wisdom systematically, on demand, for any question you wanted answered? Hanson was expanding on a key shibboleth advanced by the arch-libertarian Austrian economist Friedrich Hayek, who had argued that the prices in free markets aggregate dispersed information better than any central planner could. Hanson wanted to build tiny markets specifically designed to do that on a microscale. In 1990, he built the first corporate prediction market internally at a tech start-up called Xanadu. (Yes, the world’s first prediction market took root in a company named after a fabled imperial ruin.) Hanson spent years refining the theory, eventually getting a PhD from Caltech in 1997 and joining George Mason’s economics faculty, where he has been ever since.

In 2001, the Defense Advanced Research Projects Agency—the arm of the Pentagon that did so much to make the Internet and artificial intelligence possible—decided that his idea was worth funding. DARPA’s project was called FutureMAP (Futures Markets Applied to Prediction), and it proposed a market in which thousands of traders could bet on geopolitical events in the Middle East: coups, terrorist attacks, assassinations, regional instability. In late July 2003, Democratic Senators Byron Dorgan and Ron Wyden disparaged the program to reporters. Dorgan asked, memorably, whether the king of Jordan would appreciate discovering that the US Defense Department was taking bets on the likelihood of his overthrow within a year. FutureMAP was killed within 48 hours.

Hanson has spent the subsequent decades convinced that history will vindicate him. And now it has, in its own twisted way.

In 2018, Tarek Mansour and Luana Lopes Lara—two MIT graduates and former traders for the Citadel capital-markets firm—founded Kalshi, naming it after the Arabic phrase for “everything,” which tells you something about their ambitions and possibly their hubris. About two years later, a floppy-haired 21-year-old college dropout named Shayne Coplan founded Polymarket from what he described as his “bathroom office” during the Covid pandemic lockdown, citing Hanson as his intellectual inspiration. Kalshi was approved as a regulated exchange in November 2020 and launched publicly in 2021. Polymarket, which had opened around the same time without such approval—it’s the bad boy of the prediction-market world—was charged by the Commodity Futures Trading Commission (CFTC) in 2021 with operating an unregistered futures exchange and subsequently paid a $1.4 million fine in January 2022.

As part of the deal with the CFTC, Polymarket agreed to block American customers from using its site. But it kept operating as a global platform, albeit one run out of Manhattan, with no identity verification required because the whole thing ran on crypto, making the CFTC’s ban essentially unenforceable for anyone who knew what a VPN was. By the time Polymarket’s US ban was lifted last fall by the Trump administration’s highly sympathetic CFTC, the company was valued at $9 billion. (As of this writing, it’s still rolling out its official services in the United States.)

The Trump CFTC connection is worth dwelling on. The current agency chair, the rictus-faced Michael Selig, has proved to be an enthusiastic prediction-market fan and a resolute opponent of states’ rights, at least when it comes to regulating his precious babies. “The CFTC will no longer sit idly by,” Selig warned in one typically overheated statement, “while overzealous state governments undermine the agency’s exclusive jurisdiction over these markets by seeking to establish statewide prohibitions on these exciting products.” Selig is eagerly complicit in what is essentially a regulatory end run around state gambling laws, acceding to the industry’s redefinition of what were once called, with bracing honesty, “betting markets” as financial exchanges rather than virtual casinos. That felicitous though meaning-challenged designation allows Kalshi and Polymarket, and their legions of lesser imitators, to dodge state oversight, state taxes, and state consumer protections, and to plant their flag with a decidedly friendly federal regulator whose historical mission involved monitoring the traffic in wheat futures and pork bellies.

And that brings us to the not-so-strange case of one Donald Trump Jr., the bearded presidential failson who is a paid strategic adviser to Kalshi, an unpaid adviser to and an eight-figure investor in Polymarket through his venture-capital firm, and a director at Trump Media, which last October announced the launch of its own prediction market, Truth Predict. It’s hard to imagine a more potent symbol of an administration thoroughly in bed with an industry it is supposed to be regulating.

In any case, the grand sequel to the sports-betting gold rush is on. Robinhood—the gamified investing app beloved by pandemic-era day traders—opened its own prediction-market hub last year, where, in the interest of full disclosure, I should note that I invested in a single “yes” contract on One Battle After Another winning an Oscar for Best Picture, ultimately garnering a sweet 23-cent profit. (I didn’t fare as well in my long-shot trade on a congressional candidate in the Illinois Democratic primary, losing my entire 72-cent investment.) FanDuel, DraftKings, and Fanatics, the three giants of the sports-betting world, have all launched their own prediction-market products. This is partly, as Cohen notes, because prediction markets give them a way to operate in the handful of states, several of them huge, that still haven’t legalized sports betting—a regulatory work-around hiding inside another regulatory work-around.

Just don’t tell the titans of prediction markets that what they’re selling is gambling. “I just don’t really know what this has to do with gambling,” an exasperated Mansour told Axios. “If we are gambling, then I think you’re basically calling the entire financial market gambling.” (I’m shocked—shocked—to find that gambling is going on in this stock market!) In any case, whatever Mansour wants to call them, prediction markets are as effective a money extractor as any casino. A recent study by an equity researcher at Citizens found that prediction-market, er, traders lose proportionally more money in their first three months than do bettors on the popular online sportsbooks, with the bottom quarter of users losing about 28 cents on every dollar wagered.

But what makes prediction markets genuinely different from sports betting, and genuinely more alarming, is this: Sports betting colonized one domain—sports. Prediction markets, while still mostly devoted to sports in practice, aspire to colonize the entire information environment, and not just with omnipresent ads. CNN, CNBC, Dow Jones, and Yahoo Finance have all signed deals to integrate live odds from prediction markets into their news coverage—even though the frenzied speculation of tech bros conditioned, and now addicted, to second-guessing everything meets no existing definition of news. The Golden Globes featured Polymarket odds in its live broadcast. The vision, as Kalshi’s CEO has stated with admirable candor, is to make every difference of opinion tradable: not just sporting outcomes but politics, economics, celebrity, science, culture—anything, in short, that can be framed as a resolvable question with a clear answer. A world in which every news story has a betting button and every scroll on your phone is an invitation to wager. Call it ambient gambling.

Schüll has thought carefully about what this environment can do to the people inside it. Sports-betting apps are designed to keep users in a state of constant alertness, perpetually monitoring for the next bet; prediction markets extend this vigilance from games to reality itself. You find yourself, as she puts it, compulsively watching for tradable positions on anything and everything. “The result is a low-grade vigilance,” she tells me, an “impulsive scanning of the information environment that doesn’t switch off” even when you set your phone down. You’re not watching the news; you’re prospecting it. You’re not listening to a speech; you’re pricing it. And when everything is potentially a tradable position, as Schüll observes, something shifts in who you are in relation to the world. “You are no longer a citizen or a voter listening to a speech, or a fan watching a game,” she says. “You’re a trader.”

That brings us back to Hanson and his more ambitious sequel to prediction markets, a new system of government that he, for some reason, has decided to call by the ungainly name “futarchy.”

The core idea that Hanson has been refining since a 2000 paper whose title asks “Shall We Vote on Values, but Bet on Beliefs?” goes roughly like this: Citizens in his cartoonishly wonky version of democracy vote to determine which social and economic outcomes they want from their government in a general sense. Then prediction markets determine which policies are most likely to achieve those outcomes, and lawmakers have no choice but to act accordingly. In other words, the markets don’t just forecast outcomes; they deliver the marching orders to our nation’s bureaucrats. As Hanson explained to me, “If we could ever have markets directly advising decisions, that’s huge. Most organizations make big decisions. People make decisions. There’s just huge value at stake there.”

You may have noticed that this system seems to hand effective political power to whoever has the most money to move markets in the direction that benefits them the most. Hanson is well aware of this objection and has a ready response: Yes, very rich people could try to manipulate a decision market by betting heavily on their preferred policy outcome. But other traders, sensing a mispricing, would pile in to bet against them—correcting the distortion through the magic of market competition. The problem created by the domination of the market is solved by more market domination. When I remarked on Hanson’s logic to Cohen, he was, to put it mildly, unimpressed. “Sure. Well, sure,” he said. “Well, classic economist. Classic economist.”

In the 2013 revision of his paper, Hanson used Bill Gates as his example of the kind of impossibly rich lone wolf who still couldn’t move a prediction market against the wisdom of the crowd. In those quaint olden days, Gates was worth a mere $70 billion or thereabouts. As of this writing, our current richest dude is Elon Musk, worth upwards of $800 billion, or approximately one-fifth of the total wealth held by the entire bottom half of the American population. The math has changed, but Hanson’s opinion hasn’t.

When I noted in our sometimes passive-aggressively combative conversation that gambling on government decisions is still gambling, and gambling can cause massive harm, Hanson wanted to talk about fun—something he is very much opposed to regulating. “I myself don’t mind if people enjoy taking risks on sports betting,” he said. “It’s not for me. But they seem to have fun.”

And besides, he added, we already allow people to take enormous gambles with their lives. “We let young people decide who they date and even try to be actors or musicians,” he told me. “And those are big gambles. The overwhelming number of people who try to be musicians fail, but they seem to really enjoy it, and we decide to tolerate letting them try. So the question is just: What other kinds of fun risks do we want to let people take?” While I agree that we should let people choose who they love and what they do with their lives, I’d draw a hard line at a phone app that gives you the opportunity to lose your mortgage on your intuition about who Taylor Swift will pick as her bridesmaids.

It would be easy to dismiss “futarchy” as the fringe obsession of an economist who is genuinely a bit of a weirdo. But Hanson’s last fringe obsession, prediction markets, now powers a frenetically growing industry already worth tens of billions of dollars. The people who provide the financial backing to this industry certainly take his ideas seriously. Indeed, on the day last October that Andreessen Horowitz announced it was co-leading a $300 million investment in Kalshi, the VC firm’s editor at large Alex Danco published a blog post on its site with the intriguing title “Prediction: The Successor to Postmodernism.”

The post is, let’s say, ambitious. It argues that prediction is not merely a financial product but a new civilizational paradigm. “We create order in the universe by contributing information,” the author declares, with the calm authority of someone whose occasional blog posts earn him, well, a lot more than I’ve ever made for an article, I’m guessing. But even a peon like myself can take heart: Betting 77 cents on whether One Battle After Another would win Best Picture was, it seems, not mere speculation; it was an act of existential world-ordering. Whether all this represents philosophy in the service of capital, or capital in the service of philosophy, is left unclear. What is clear is that no one involved seems to find the distinction particularly important.

Marx and Engels famously warned that the rise of the capitalist class would leave “no other nexus between man and man than naked self-interest, than callous ‘cash payment,’” plunging every aspect of our lives into “the icy water of egotistical calculation.” The prediction-market faithful are gleefully jumping into this cold bath. The last thing that hadn’t been financialized—human thought itself, the act of holding an opinion, the experience of disagreeing—is now a tradable asset with a fluctuating price. Every belief liquefies into a contract. All that is solid melts into Kalshi.

Or does it? The outcome is hardly preordained. Consider: The more experience people have with online sports betting, the less they like it. A Pew survey in the summer of 2025 found that 43 percent of Americans thought that legal sports betting was bad for society, up from 34 percent in 2022. Most striking of all: 47 percent of men under 30 said it was bad for society, up from a mere 22 percent in 2022. That is, the demographic that the industry has targeted the most aggressively and damaged the most severely are turning against it the most dramatically.

And since most people’s introduction to prediction markets is headlines about insider trading on war and death, it seems likely that people could sour on them even more quickly. If this trend line continues, we may be able to slow down, and possibly even shut down, their spread before they reach the ubiquity of sports betting—much less the cultural and political omnipresence that Hanson and the other prediction-market ideologues dream of. Early reports are encouraging. A 2026 survey by Ipsos for the American Institute for Boys and Men found that 61 percent of Americans see prediction markets as more like gambling than investing; only 8 percent buy the industry line that they’re investment vehicles. Even more striking, only a scant 4 percent see them as good for society. (Cohen is a policy official for the institute.)

Even Hanson can see the storm clouds forming. “There’s a risk that it will cause a backlash,” he told me, “in which case my vision will be delayed. But I’m hopeful, at least at the moment, that they won’t face too severe a backlash too soon.” I wouldn’t take that bet.

The legal war is already under way. Kalshi alone faces more than 20 federal and state lawsuits, with attorneys general from Nevada to Michigan to Massachusetts filing complaints advancing the same basic argument: that prediction markets are gambling platforms wearing the mask of a financial exchange, and that states have every right to regulate them as such. In March, Kalshi was criminally charged by the attorney general of Arizona with operating an illegal gambling business. Addressing CFTC head Selig directly in an X post, the Republican governor of Utah, Spencer Cox, quipped that he didn’t remember “the CFTC having authority over the ‘derivative market’ of LeBron James rebounds. These prediction markets you are breathlessly defending are gambling—pure and simple.” He continued in a darker vein: “They are destroying the lives of families and countless Americans, especially young men. They have no place in Utah.”

Congress is stirring, too. Senators have introduced a small flurry of bills targeting prediction markets, ranging from Connecticut Democratic Senator Richard Blumenthal and his New Jersey colleague Andy Kim’s comprehensive Prediction Markets Security and Integrity Act—which would ban war-and-death contracts, impose insider-trading rules, and return regulatory power to the states—to a bipartisan bill sponsored by Democratic Senator Adam Schiff of California and Republican John Curtis of Utah that would ban sports betting on prediction markets, a move that could deprive Kalshi of 90 percent of its revenues. “Nobody should be making bets on if the United States is going to war or what words President Trump is going to use in a speech,” said Senator Chris Murphy, whose own bill would ban trades on nonfinancial government actions and events for which some people know the outcome in advance. “Those are fundamentally corrupt markets, because there are people on the inside who know the answer, and it perverts the decision-making process.”

Harry Levant, who has spent the last decade watching a gambling industry promise responsible behavior while delivering the opposite, is under no illusions about how quickly this gets fixed. “The public’s going to win this debate,” he told me. “The question is how long it takes.”

Support The Nation’s June Fundraising Campaign

With the midterm elections now firmly upon us, the question is whether Democratic candidates will do more than merely occupy ballot lines as mild alternatives to the red-hot crisis that is Donald Trump.

As Trump spends over $1 billion a day on a globally destabilizing war on Iran and admits that he doesn’t “think about Americans’ financial situation,” millions across the country are struggling with the surging costs of essentials. Democrats must seize this moment and advance bold, small-“d” populist ideas—not settle for cynical caution that once again snatches defeat from the jaws of victory.

The Nation elevates progressive ideas, movements, and elected officials achieving real change across the country into the national conversation. At the same time, our journalists are exposing how crypto and AI-funded super PACs are spending hundreds of millions of dollars to knock out candidates they oppose, reporting on the devastating impact of the Supreme Court’s evisceration of the Voting Rights Act, and sounding the alarm on attempts by red states to quickly redraw electoral maps, disenfranchising Southern Black voters.

We can play this critical role because of support from readers like you. This June, we’re raising $20,000 to power The Nation’s independent journalism in the run-up to November’s immensely consequential elections.

It’s in our power to build a more just society, and your support at this critical moment brings us closer to that bold vision. I hope you’ll donate today.

Onward,

Katrina vanden Heuvel

Editor and Publisher, The Nation

More from The Nation

The Supreme Court Once Again Endorses Trump’s Racism The Supreme Court Once Again Endorses Trump’s Racism

The court took a look at Trump's obviously bigoted handling of the Temporary Protected Status program and said, “Nothing to see here.”

Arab Americans Have Always Been Here Arab Americans Have Always Been Here

The story of my people, and my country.

How I Became an American How I Became an American

My path to US citizenship was a long and difficult one.

The World Cup of Racism The World Cup of Racism

The Trump administration has a message for every soccer fan on the planet: The US government is unapologetically bigoted.

The Supreme Court Loves Religious Freedom—Just Not for Rastafarians The Supreme Court Loves Religious Freedom—Just Not for Rastafarians

In a far-reaching ruling, the court violated a man’s constitutional rights—and undermined fundamental civil rights protections.

250 Years of Genocide, Theft, and Displacement 250 Years of Genocide, Theft, and Displacement

Natives have nothing to celebrate as the United States stages another sick-making festival of self-congratulation.