How Israel Bonds Put the Cost of the War in Gaza on US States and Municipalities

After October 7, Palm Beach County, Florida, bought $660 million in Israel bonds. A new lawsuit argues that it’s a bad deal for taxpayers.

The Israeli Finance Ministry has estimated the per diem cost of its government’s unremitting attacks on Gaza as $270 million. By midsummer, Israel is projected to have spent $50 billion, more than 10 percent of the nation’s total GDP. The Israeli government has taken on these costs by relying heavily on debt financing. The strategy is as old as the country itself.

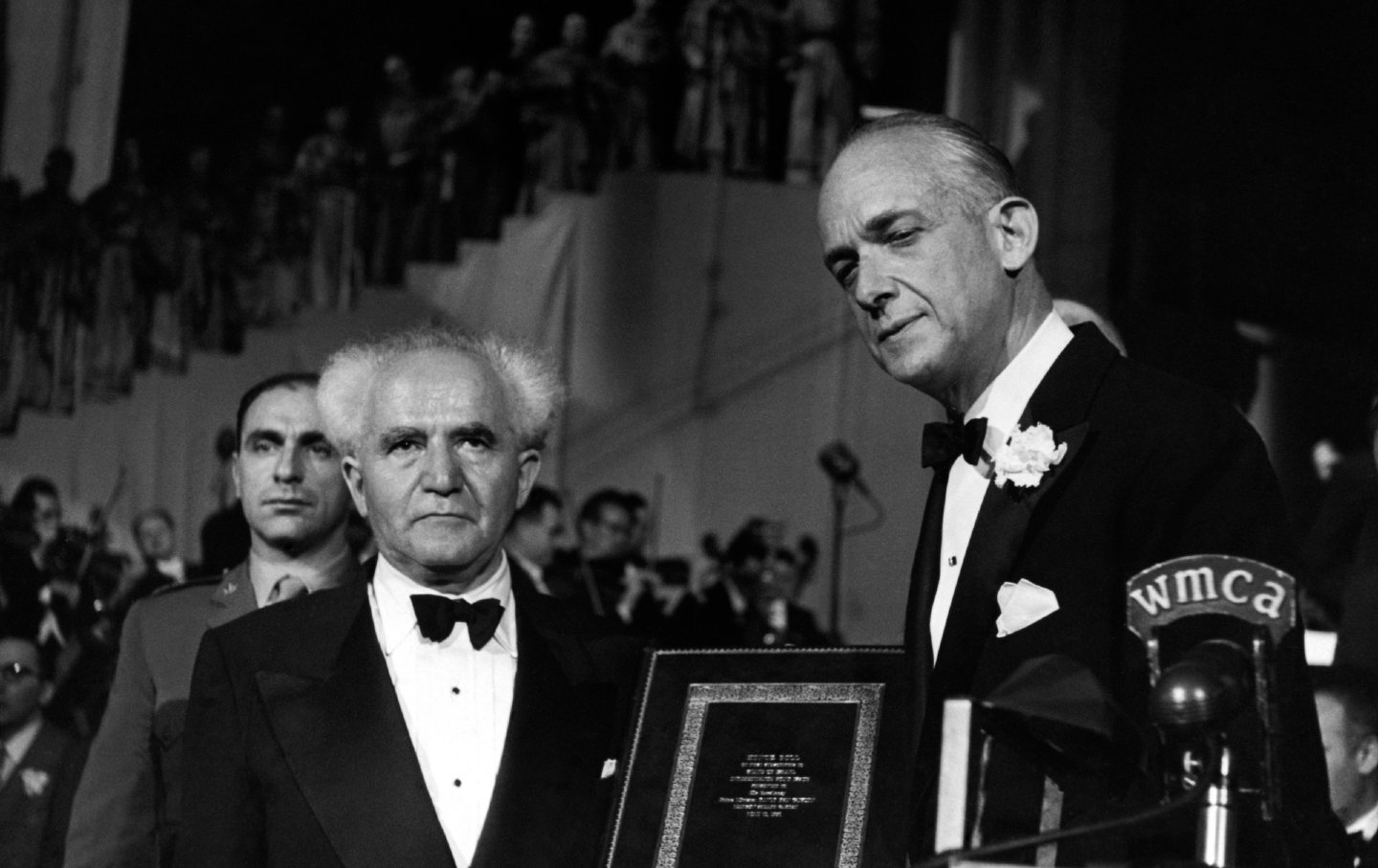

In 1951, on the heels of the 1948 Arab-Israeli War, known by Palestinians as the Nakba, Israel’s first prime minister, David Ben-Gurion, traveled to Madison Square Garden to inaugurate the sale of Israel bonds to American investors. Some $35 million of bonds—the present-day equivalent of almost half a billion dollars—were bought that day by individuals and institutions.

Israel Bonds—formally, the Development Corporation for Israel—the company that underwrites these bond sales, has played a central role in the development of the Israeli state, and, importantly, in financing the costs of ethnically cleansing and illegally occupying historic Palestine.

Israel bonds are state-issued securities—comparable to US savings bonds—that the Israeli government sells to support general spending. The money from the bonds is deposited directly into the “general budget” for the State of Israel. The capital raised is not earmarked or publicly disclosed. As money in the Treasury, the funds are currently under the control of far-right Finance Minister Bezalel Smotrich—a man who recently called for “no half jobs” regarding the “total and utter destruction” of Gaza.

Israel bonds have long been popular gifts and investments purchased by the Jewish diaspora, often given as birthday or bar- or bat-mitzvah presents; the different series of bonds, themselves, are sold under titles like Jubilee and Mazel Tov. Yet it is American states and municipalities that have emerged over the past 20 years as a primary investor in these sovereign bonds.

In the six months following the Hamas attack, at least 14 states and four municipalities invested in Israel bonds. Their total holdings, as of February 2024, amounted to $1.6 billion.

This swell of support, despite a shrinking Israeli economy, illustrates how Israel bonds have more in common with war bonds than with standard Treasury bills. Historically, Israel bond sales have spiked dramatically with each conflict dating back to the nation’s establishment, and, like war bonds, there is no secondary market—meaning the bonds are held by their original purchasers until maturity. Without the ability to trade, the buyer is tied to the bond regardless of market or political conditions. This intentional feature of the bond signals the commitment of the investor to the project of Israel, not necessarily to their own profit maximization.

Moreover, an analysis by Duke University’s Michael Bradley found that Israel bonds act, essentially, as a countercyclical debt instrument: allowing the country to maintain a constant level of spending amid war-induced recessions. It is a process historically dependent on what is called the “patriot discount,” whereby investors knowingly accept below-market returns in an act of nationalistic altruism. In times of conflict, Bradley concludes, investors in Israel “give more and take less.”

Palm Beach Florida Residents File Lawsuit Demanding Divestment

Last Wednesday, May 22, residents of Palm Beach County filed a groundbreaking lawsuit alleging that the county comptroller and clerk of the Circuit Court, Joseph Abruzzo, violated his fiduciary duty by investing $660 million of local tax revenues in Israel bonds in the months following the October 7 attack.

On September 30, 2023, the end of the fiscal year and just days before the Hamas attack on Israel, Palm Beach County held just $40 million in Israel bonds. At the time, this represented about 1 percent of Palm Beach County’s total portfolio. Yet, over the next six months, Abruzzo made a series of investments adding up to a total of $700 million of taxpayer dollars in Israel bonds. The comptroller’s office described the investments as a “show of support for Israel following their declaration of war against Hamas militants.”

Abruzzo’s spending spree transformed Palm Beach County into the single largest holder of Israel bonds in the world. The investment now represents 15 percent of Palm Beach County’s $3.6 billion investment portfolio.

The lawsuit alleges that these investments constitute a violation of Florida Statute 218.415(24)(b), which mandates that “[t]he unit of local government must make decisions based solely on pecuniary factors and may not subordinate the interests of the people of this state to other objectives.” Ironically, this statute, passed just a year ago, was championed by conservative governor Ron DeSantis as a way to forestall any state investment considerations of ESG, or green, bonds.

The timing of Abruzzo’s investments, and his many public statements supporting Israel, reveal the openly political character of these decisions. And Abruzzo is not alone. As the Israel’s bombing campaign ramped up this fall, the Texas State Treasury invested $65 million in Israel bonds, Illinois added $10 million, Indiana bought $35 million, Florida put down $145 million, and the New York Common Retirement Fund invested $20 million, among a handful of other multimillion-dollar purchases across the county.

Investing in Genocide

The lawsuit in Palm Beach painstakingly outlines the various ways that Israel’s economy has been suffering, not only since the October 7 attack but beginning in January 2023 when the Israeli Knesset passed legislation limiting the Supreme Court of Israel’s power. That legislation and the ensuing protests were viewed as evidence of political instability in the country, and within a few weeks an estimated billion dollars had left the country. The lawsuit notes Israel’s contracting GDP, struggling stock market, negative credit ratings and outlooks, and a ballooning deficit. Still, it came as no surprise when state and municipalities stepped in to buoy the flailing economy.

Unlike these public investments, the Wall Street institutions floating money to Israel as part of the country’s recent conventional bond sales refused to take such risks without charging additional fees.

These deals, made behind closed doors, are often referred to as “private placement” because the terms of the bond sales are never made public; the arrangement allows Israel to circumvent writing a bond prospectus—the legal document regulated by the Securities and Exchange Commission (SEC) that details all investment risk factors. It also allows Israel to keep hidden the fees paid out. In fact, the SEC hasn’t published a prospectus from Israel on this class of bonds since 2018.

If Israel did issue a new prospectus, it would be forced to disclose the reality of its current economic and political difficulties—or become exposed to legal liability for fraud.

Instead, Israel prefers to pay over $100 million in placement fees to Bank of America and Goldman Sachs to avoid international investor scrutiny.

Popular

“swipe left below to view more authors”Swipe →From Endowments to Bonds

The renewed focus on Israel bonds comes on the heels of a nationwide student movement demanding that universities divest their endowment portfolios from companies in Israel. Few of these student campaigns have been successful thus far—though not for lack of effort.

Part of the reason may be the financialization of university endowments that has distanced the schools from their investment portfolios, often managed by private financiers and spread thinly across index and mutual funds. Universities facing such calls for divestment have hidden behind the opaque nature of their investment portfolios.

Unlike universities, states and municipalities are under a legal obligation to report their investments. And those in charge of these funds, like Abruzzo, hold a fiduciary duty toward their constituents, whose taxes they are investing. States, municipalities, and pension funds were successfully pressured into divesting from apartheid South Africa, ultimately passing resolutions to do so. Norway made international headlines when the nation’s pension fund divested its entire Israel bond holdings, citing “uncertainty in the market.”

Cracks in the Armor

As Israel continues its all-out war, the country is becoming further isolated and destabilized. Shifts in the political consensus are emerging: Ireland, Spain, and Norway have now recognized Palestine as a sovereign state.

On May 20, the chief prosecutor of the highest international criminal court issued a request for arrest warrants for Israeli Prime Minister Benjamin Netanyahu and Israeli Defense Minister Yoav Gallant. The two officials stand accused of international war crimes ranging from employing “starvation as a method of warfare” to “extermination.” A panel of three judges will soon decide whether to issue these warrants. On May 24, the International Court of Justice, which is currently deciding South Africa’s genocide case against Israel, ordered Israel to “immediately halt its military offensive” in Rafah. In the days following these court orders, Israel has brazenly continued to target civilian encampments in Gaza, with strikes leading to a deadly fire on Monday.

The lawsuit in Palm Beach will likely be just the first of a wave of forthcoming legal challenges to Israel bonds. As it stands, American taxpayers are being forced to buoy the Israeli economy as it brutalizes Palestinians from Gaza to the West Bank; but the alliances that hold this arrangement together are more precarious than they appear.

More from The Nation

Paying Tribute to Richard Lingeman—Longtime Executive Editor and a Quiet Force at “The Nation” for More Than Three Decades Paying Tribute to Richard Lingeman—Longtime Executive Editor and a Quiet Force at “The Nation” for More Than Three Decades

A man of few spoken words, on the page he was a marvel.

Root for Spain for Their Play and Their Politics Root for Spain for Their Play and Their Politics

A World Cup victory will not just feel like a soccer triumph but a national triumph. For that reason, fans should support Pedro Sánchez’s Spain over Javier Milei’s Argentina.

What We Can Learn From the Current Menopause Moment What We Can Learn From the Current Menopause Moment

At a time when the Trump administration is endangering women’s health, more than half the states, red and blue alike, have introduced menopause legislation.

Golf Caddies Just Unionized for the First Time Golf Caddies Just Unionized for the First Time

Caddies—workers tasked with everything from carrying golfers’ bags to giving them armchair therapy—won out after a recent change to their employment structure.

When Will Cancer Stop Being “Our Fault”? When Will Cancer Stop Being “Our Fault”?

By placing the burden of maintaining one’s health on individuals, we obscure the broader environmental, political, genetic, and social forces that affect our well-being.

How One Woman Is Using the UN to Attack Trans Rights Worldwide How One Woman Is Using the UN to Attack Trans Rights Worldwide

It’s no coincidence that the Supreme Court’s decision allowing trans sports bans echoes the work of Reem Alsalem, the UN special rapporteur on violence against women and girls.