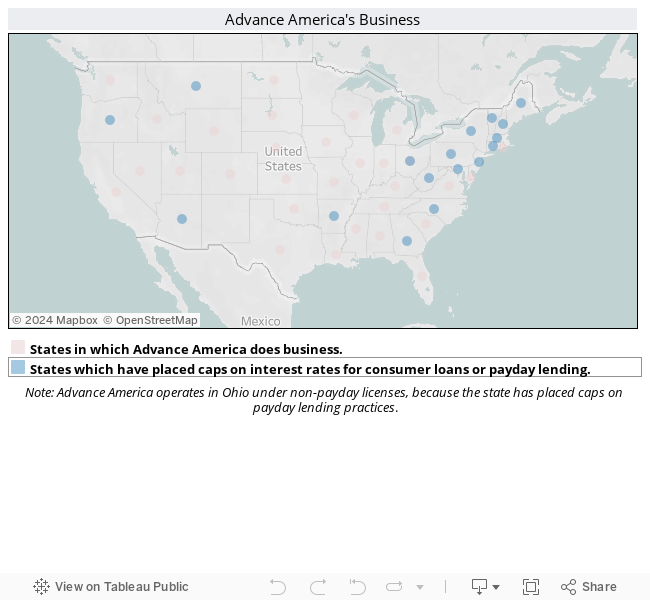

Advance America’s business model depends on exploiting the largely unregulated payday loan market. But there are 17 states that have placed a cap on interest rates for consumer loans broadly or payday lending specifically (Washington, D.C. has also placed caps on interest rates). In all of those states, Advance America does not do business, with the exception of Ohio, where it operates under non-payday lending licenses. For more on Advance America and payday loans, read Kai Wright’s Bad Credit: How Payday Lenders Evade Regulation.