Despite Wall Street’s recent gains, the foreclosure crisis that displaced 10 million Americans continues to wreak havoc on communities. One ongoing problem is that 10.7 million homeowners are stuck in underwater homes, in which the mortgage is more than the house is currently worth. Although the federal government doled out $700 billion to Wall Street via TARP during the 2008 financial crisis, it has not taken bold action to solve this problem. Money set aside during the bailout to help homeowners remains largely unspent, and a key federal housing regulator refused to pursue mortgage write-downs for struggling borrowers, even though their own analysis showed these loan modifications would save the agency money.

In this vacuum, several cities have begun to take matters into their own hands, as Peter Dreier reported on for The Nation. One plan by private equity company Mortgage Resolution Partners proposes that cities use eminent domain—a power traditionally reserved for seizing property for public use—to seize mortgage loans. The amount owed on the loans would then be reduced so that the borrower was no longer underwater, avoiding foreclosure. In January 2013, Brockton, Massachusetts commissioned a study and formed a working group to investigate using eminent domain to help struggling homeowners. In September 2013, the city council of Richmond, California, voted to move forward with such a plan.

One might think these small, local efforts shouldn’t be of much concern to Wall Street—after all, Richmond’s plan affects a mere 624 loans. But one of Wall Street’s most powerful trade groups, the Securities Industry and Financial Markets Association (SIFMA), has responded with ferocious urgency. SIFMA is the attack dog the largest Wall Street banks send when they don’t want their names attached to politically controversial lobbying efforts or lawsuits. The group does everything from denying that “too big to fail” still exists to drafting lengthy comment letters arguing for weaker financial regulation.

New e-mails obtained through a Freedom of Information Act request by the Alliance of Californians for Community Empowerment (ACCE) and a coalition of other community groups and shared with The Nation reveal the extent to which SIFMA has been spearheading Wall Street’s fight against using eminent domain to mitigate the foreclosure crisis. (The complete set of e-mails are available at the website of the ACLU, which sued the FHFA when the original FOIA request was ignored). When Brockton began considering using eminent domain, SIFMA employees traveled there and kept an entire section of its website, complete with an array of resources, to decrying the plans.

Popular

"swipe left below to view more authors"Swipe →

Grace Ross, Coordinator of the Massachusetts Alliance Against Predatory Lending and one of the members of Brockton’s eminent domain working group, said she was “shocked by the huge amount of resources SIFMA threw at this small study process in Brockton. While pursuing a plan like this would be deeply meaningful to Brockton, with up to 2,300 households that could have been directly affected, it’s small potatoes” for an industry as large as Wall Street. In April 2013, by a vote of 7-5, Brockton’s eminent domain working group concluded that the City did not have the legal authority to pursue an eminent domain plan.

SIFMA also made sure to send its careful notes and observations to a key staffer at the Federal Housing Finance Agency (FHFA), General Counsel Alfred Pollard. The FHFA is the regulator who oversees Fannie Mae and Freddie Mac, which have been under federal government control since the 2008 financial crisis. In 2008, Congress also charged the FHFA with implementing “a plan to maximize assistance for homeowners.” But not only has FHFA failed to meaningfully help homeowners, in an August 2013 statement, the agency threatened to take legal action against localities that used eminent domain to restructure mortgages, and it raised the possibility that Fannie Mae and Freddie Mac would be ordered to stop doing business altogether in areas that pursued eminent domain plans.

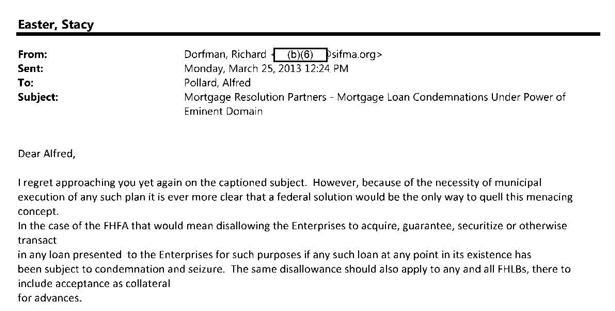

Through e-mails obtained by the ACCE’s FOIA request, we now know that SIFMA urged the FHFA to take precisely this course of action. In a March 25, 2013, e-mail to FHFA’s General Counsel Pollard, Richard Dorfman, then-head of SIFMA’s Securitization group, writes that “a federal solution would be the only way to quell this menacing concept.” Dorfman goes on to insist that the FHFA disallow Fannie Mae and Freddie Mac “to acquire, guarantee, securitize or otherwise transact in any loan” that could even hypothetically be subject to an eminent domain plan. And that is exactly what the FHFA did four months later.

In response to a request for comment on whether SIFMA’s e-mails influenced the FHFA’s actions, an FHFA spokesperson said, “FHFA first expressed concerns about the use of eminent domain when it requested public input on August 8, 2012.” The spokesperson noted that the August 2013 statement “reflected FHFA’s analysis of input provided, legal matters, and safety and soundness concerns for its regulated entities (Fannie Mae, Freddie Mac and the 12 Federal Home Loan Banks).” The spokesperson also said that the statement was “influenced by legal research and robust public input, including 75 letters from a variety of stakeholders.”

But SIFMA did not stop at demanding the FHFA’s help in threatening cities that pursued eminent domain mortgage seizures; it also asked FHFA staff to drum up local opposition. In the March 25 e-mail to Pollard, Dorfman writes, “Councilor Tom Brophy…is a key participant in the eminent domain working group in Brockton. [He] wants to speak with you by telephone pertinent to the matters I have raised…. I am accordingly asking you to agree. Please agree to do so, and we will make the arrangements.”

Brophy ultimately voted with the majority to scuttle the eminent domain plan on the grounds that Brockton did not have the legal authority to seize mortgages. Reached for comment, Brophy said that he does not recall any specific conversation with anyone from the FHFA, and the FHFA declined to comment on whether or not Pollard and Brophy ever talked on the phone. Whether or not that particular conversation took place, however, the e-mails reveal the active role SIFMA took in lobbying federal agencies to intervene in the Brockton vote, and they raise a question about how much influence SIFMA had on the outcome.

In addition to the comfort level displayed in their requests, the sheer volume of e-mails from SIFMA employees to General Counsel Pollard is significant. There is a formal comment process, yet SIFMA appears to have the capacity to supplement this process with these informal, previously private, e-mails to Pollard. When asked if e-mailing General Counsel Pollard directly is something that is available to all stakeholders, an FHFA spokesperson noted, “The Office of General Counsel email address is available to all stakeholders on the FHFA website.” But the e-mail provided on that website is [email protected]. In the FOIA response, the e-mail used by SIFMA to contact Pollard is different: [email protected].

The FHFA spokesperson also stated, “FHFA’s General Counsel routinely communicates with a variety of interested parties on numerous issues affecting Fannie Mae, Freddie Mac and the Federal Home Loan Banks.” Of the personal e-mails revealed by the FOIA, twenty-four are from SIFMA, and the rest are primarily from other Wall Street stakeholders (The additional listed documents are court filings or public comment letters—some of which were sent via e-mail and are thus listed as “comment e-mails”). And while the October 2013 FOIA did ask specifically for e-mails between Wall Street stakeholders and FHFA, it also included a much broader request for “all documents,” correspondence and meetings “regarding the City of Richmond’s offer to buy underwater mortgages from residents.” One would expect to see e-mail exchanges to Alfred Pollard from non–Wall Street stakeholders about Richmond, if FHFA truly had as close a relationship with others as they appear to have with SIFMA.

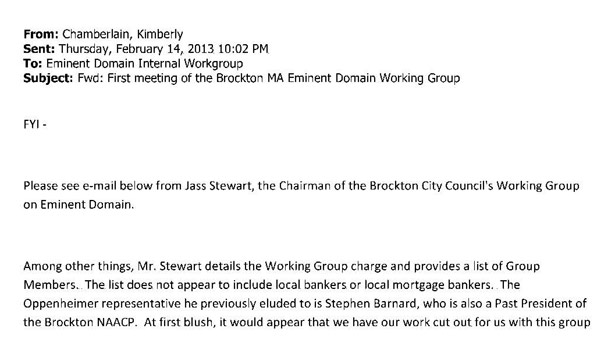

Perhaps one of the most damning e-mails is one forwarded to Pollard by SIFMA’s Dorfman on February 15. In it, Kimberly Chamberlain—managing director and associate general counsel of state government Affairs at SIFMA—laments the lack of bankers on Brockton’s Eminent Domain Working Group. Chamberlain concedes that there is an Oppenheimer representative, Stephen Bernard, on the working group. But it appears that to Chamberlain, Bernard’s industry credibility is in question, due to his association with the NAACP. Chamberlain writes, “The list does not appear to include local bankers or local mortgage bankers. The Oppenheimer representative he previously alluded to is Stephen Barnard [sic], who is also a Past President of the Brockton NAACP. At first blush, it would appear we have our work cut out for us with this group” [emphasis added].

It remains unclear why an affiliation with the NAACP is relevant for SIFMA to note, especially before stating that “this group” will require more work on their part. In response to a request for comment on the e-mail, a SIFMA spokesperson stated: “The e-mail from Ms. Chamberlain simply restates the information in Mr. Stewart’s original e-mail, which notes the affiliations of the working group members. SIFMA had been told, prior to the working group being formed, that the group would include several financial services representatives who could speak firsthand about the negative impact of eminent domain on mortgage credit. Without this firsthand experience, SIFMA felt it would be important to spend time educating working force members.”

In some e-mails, SIFMA also appears dismissive of the scale of the foreclosure crisis. In the March 25 e-mail, Dorfman calls the eminent domain plans “tedious.” In a March 8 e-mail to Pollard, Chris Killian, managing director and head of securitization at SIFMA, insults Brockton’s eminent domain committee, writing “the current ‘committee’ carries many markings of a charade.”

SIFMA’s concern is not the plight of these cities—but rather the time and money SIFMA has lost fighting eminent domain plans. In the February 15 e-mail, Dorfman writes to Pollard about eminent domain plans in Brockton and in Phoenix, Arizona: “One of the City Council members has found a messianic calling in the eminent domain scheme, so we are once again investing time and resources in this matter,” time that he laments should instead be focused on the “flurry of regulatory activity derived from Dodd Frank.”

The re-focusing of SIFMA’s attention from federal regulations to the actions of a few small cities trying to creatively solve their foreclosure crisis tells us that these eminent domain plans are a significant threat to Wall Street. SIFMA is terrified that this idea will spread. As SIFMA’s Killian wrote on March 8, “one of these places where there is smoke will soon catch fire.” If there is one thing SIFMA does not want, it is for banks to have to go to court, in multiple cities, to try and fight seizures of mortgages via eminent domain.

As of January 6, 2014, the FHFA has a new head—Mel Watt, who until recently served as a Democratic Representative from North Carolina. SIFMA has hardly made it a secret that it is expecting Watt to continue FHFA’s war on eminent domain plans. When Watt’s nomination was first announced, SIFMA released a statement insisting Watt “explicitly address the continued threat” of plans using eminent domain to seize mortgages. One of the first questions the public should ask is: Will the FHFA under Watt continue this tradition of using its power to act as a proxy for SIFMA? Or will Watt support cities’ searching for new and novel approaches to foreclosures?

Given that it’s been five years since the crisis and the federal government has done appallingly little to help homeowners, the least the FHFA could do is stay out of the way.