Donald Trump, it seems, has never met a conflict of interest he couldn’t immediately embrace. The emolument clause? Not his problem. Hosting Richie Rich types at Mar-A-Lago? The club’s membership fee doubled shortly after Trump was elected president.

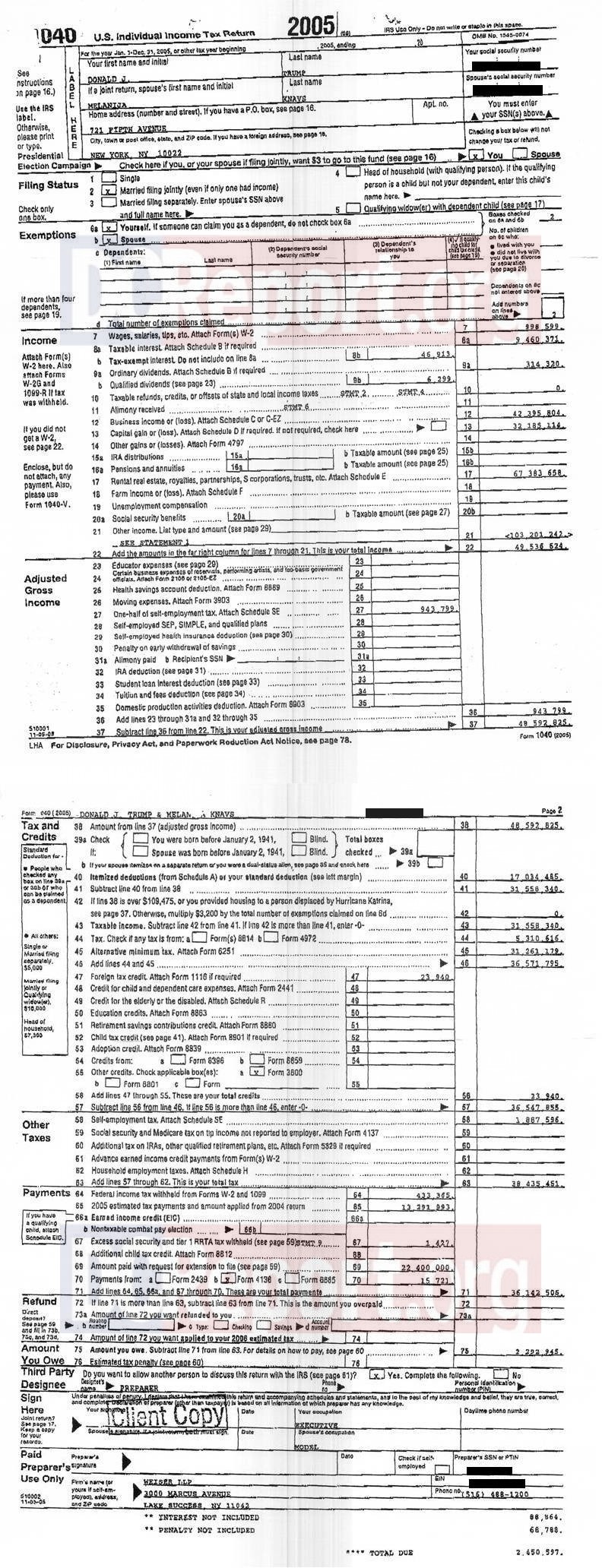

So it should come as no surprise to discover that Trump’s distaste for the alternative minimum tax (AMT), which his tax-reform package would eliminate, might well be more than a bit personal. According to a two-page excerpt from Trump’s 2005 taxes mailed anonymously to Pulitzer Prize–winning investigative reporter David Cay Johnston and published Tuesday by DCReport.org, Trump’s income that year was slightly more than $150 million. In turn, Trump paid about $38 million to the Internal Revenue Service.

Without the alternative minimum tax, Trump would have owed significantly less money to the feds—about $5 million on his earnings, and almost $2 million in self employment taxes. If you don’t count the latter sum, Trump would have been taxed at an effective rate of about 3 percent, putting him in a tax bracket that doesn’t exactly scream mildly affluent, never mind one befitting a man who claims to be worth $10 billion. As Johnston helpfully explained on MSNBC, “If we didn’t have the alternative minimum tax, he would have paid taxes at a lower rate than the poor who make less than $33,000 a year.”

Poor Donald! He was snagged by a tax designed to snag people just like him.

The alternative minimum tax originated in 1969, during the Richard Nixon administration. After a study was published showing 155 wealthy people earning more than $200,000 (about $1.3 million today when adjusted for inflation) paid no taxes at all thanks to a number of deductions and loopholes, Congress took action. The result? A minimum tax, a surcharge paid by wealthy filers. Legislation enacted in the late 1970s and early 1980s changed that to the alternative minimum tax as we now experience it.

But while the method for calculating federal tax brackets was indexed to inflation, the alternative minimum tax was not. Eventually, people who felt they were not wealthy were getting dinged by the AMT. According to the American Enterprise Institute, less than 1 percent of taxpayers got hit by the AMT in 2000, a number that tripled to 3 percent by 2008. Many other taxpayers would likely have been subjected to it, but Congress routinely passed temporary time-limited fixes, before finally indexing the AMT to inflation permanently in 2012. But that still didn’t make it popular. A lot more people than Congress originally intended pay the ATM, after all. The Tax Policy Center, a joint initiative of the Urban Institute and the Brookings Institution, estimates 4.8 million taxpayers will pay the AMT in 2017.

Popular

"swipe left below to view more authors"Swipe →

No doubt the way the AMT works makes it such a popular punching bag. Many tax filers are required to work out their tax bill twice, once using conventional means, the second time for the AMT. If they face a higher bill under the latter method, they owe more money. This results in the loss of deductions such as ones for state and local taxes, property taxes, dependent exemptions, and miscellaneous business and investment expenses such as paying an accountant to prepare the taxes. Deductions for medical expenses also go by the wayside. (Charitable donations are still deductible, as is mortgage interest.)

It’s easy to view this as not exactly fair. You don’t need to be Donald Trump to find yourself caught in the cross hairs of the AMT. As I mentioned in the last paragraph, you might suffer from ill health, have several children, or simply reside in a high-tax state—people living in New York, California, New Jersey, or Massachusetts are more likely to be subject to an ATM bill than those living in lower-tax jurisdictions. As a result, anti-AMT sentiment makes for surprising political bedfellows. “The AMT, combined with rising property and other taxes, is yet one more cost making it harder for the middle class to make ends meet,” the Staten Island Advance, the paper of record for the only New York City borough where voters were more likely to favor Trump over Hillary Clinton, opined last month. But Bernie Sanders has also proposed ending the AMT as part of his tax-reform package. David Cay Johnston isn’t a fan either. He calls it “immoral.”

Yet at the same time, there is some truth to the argument made by others that much of the caterwauling about the AMT is done by people who don’t want to acknowledge their relative privilege:

https://twitter.com/jbarro/status/841833160321187840

https://twitter.com/jbarro/status/841833288444608512

The AMT is a tax that impacts the upper middle class—the sort of people who are most likely to, say, buy a home with a five-figure property-tax bill. According to the Tax Policy Center, households with incomes between $500,000 and $1 million are significantly more likely to pay the alternative minimum tax than those with earnings above that threshold, in part because people earning seven-figure sums are likely paying taxes at a rate higher than then AMT would charge. The AMT arouses rage because, in many cases, these are not people who perceive themselves as wealthy—though they might well be, just not in comparison to Trump who, do I need to mention again, apparently earned about $150 million in 2005.

Nonetheless, there are almost certainly better ways to get the wealthy—no matter how you are defining them—to pay their fair share. As Mark Green wrote in The Nation in 2007, we could instead tax capital and income at the same rate. The so-called Buffett Rule, which Barack Obama pushed, would have imposed a tax rate of at least 30 percent on those earning at least $1 million a year could also make a difference. Johnston, in a 2013 interview with Forbes, suggested possibly rejiggering the AMT so that it began to impact people at a “high income threshold” like $500,000, as well as not counting things like deductions for household members and state and property taxes in the calculation.

All of these plans sound reasonable. But Donald Trump isn’t advocating for them. He’s advocating for a tax reform that would almost certainly benefit him enormously, at least by the evidence presented by his 2005 returns. At best, he is a bad spokesman for the cause. At worst, he’s once more using the presidency as a way to personally make a buck—in this case, apparently lots of them. As my mother likes to say, people don’t change.

And, oh, you are wondering, what do the taxes themselves tell us? Not much. For that we would need the various schedules used to compute the taxes, which were not leaked to Johnston. We would also need to see his corporate taxes.

{kind=link}